These venture rounds would get the companies through Phase 1, or at least most of preclinical development. COGS is cost of goods sold (manufacturing plants, personnel, raw materials, etc.). I used a "blended" discount rate rather than just using the acquiror's or target's discount rate. This course assumes no prior knowledge in biotech company valuation. Most AI programs involve using AI in the "target-to-hit" stage, and some can also do hit-to-lead and lead optimization work. The Pharma-Biotech Valuation Model Template calculates the risk-adjusted DCF (Discounted Cash Flow) Value of a Pharma or Biotech Company. Drugs become much more valuable. WebIn 2018, 66% of Series A investments were in discovery or preclinical-stage companies. Pharmacology focuses on the study and development of medicine, drugs, etc. Because these diseases affect so few patients, there has historically been less research into these diseases compared to more prevalent conditions. The post is accompanied by two tools that can help you apply this knowledge: an interactive drug valuation calculator and an excel spreadsheet with an example of how a drug company might be valued. Consider the most prominent 2017 biotech M&A deal when Gilead bought Kite Pharma for almost $12 billion. WebValuate is a Microsoft Excel spreadsheet template for establishing a reasonable royalty rate and license issue Luehrmann for the University of California.

Second, this scenario tree stops post NDA approval, but one could conceivably develop scenarios for the post-approvali.e., revenuestage, too. Analysts typically focus on market potential in the industrialized countries, where people will pay the market price for drugs. Build sophisticated biotech DCF models in the browser. If there is a competitive drug market, with limited advantage offered by the new drug in terms of increased effectiveness or reduced side effects, the drug will probably not win substantial market share in its product category. Uploaded by w_fib. Nature Biotechnology. By deducting the drug's operating costs, taxes, net investment and working capital requirements from its sales revenues, you arrive at the amount of free cash flow generated by the drug if it becomes commercial. This model tries to do it all, with all of the associated risks and rewards. In other words, it estimates the current value of a business based on its expected future cash flow. Consider the most prominent 2017 biotech M&A deal when Gilead bought Kite Pharma for almost $12 billion. During lead optimization, the most promising hits are further optimized. WebBiotech Valuation Idiosyncrasies and Best Practices. These are some of the most-cited studies of the costs of drug development. EFinancialModels provides a broad range of industry-specific monetary model templates in Excel. This article examines how to value such pipelines. Medical Device tools for diagnosing, prevention, treatment, etc. Scribd is the world's largest social reading and publishing site. Biotech companies are uniquely situated types of investments that can either pay off handsomely or end with little to show for it, making them quite risky. After all required testing is completed, companies submit to FDA an application for approval, complete with detailed reports and data from all relevant studies. Which is not too far off from the market. Especially with the advent of the first approved gene therapies, this is now an increasingly relevant possibility. As institutional equity investors, its clear that this cannot be simply explained by the exuberance of investors. This Excel spreadsheet template contains a great set of useful tools to better understand the value of a Pharma or Biotech company. This spreadsheet template may be used and duplicated by anyone as long as (1) this entire paragraph is appended to all copies of this spreadsheet template and (2) the similar  This drug price yields an NPV of 0 at the start of the project, and thus is the minimum drug price that would attract investment, given our assumptions about the cost of development. However, while valuation may appear to be more guesswork than science, there is a generally accepted approach to valuing biotech companies that are years away from payoff. Biotech companies with little to no revenue can still be worth billions. These, of course, are the most general base rates we could use and we should and can be enhanced by taking into account the therapeutic area or novelty of the drug candidate, as shown in the following graphs from Bank of America Merrill Lynch: There are further potential adjustments to the base rate one could come up with, even such that do not have anything to do with the drug itself, such as the track record of the company (its R&D and regulatory teams) in getting drugs approved. WebValuation and Deal Structuring - Biotechnology Innovation Organization In fact, cash flows prior to approval of a drug will be significantly negative. This Excel spreadsheet template contains a great set of useful tools to better understand the value of a Pharma or Biotech company. The time to peak sales reflects the fact that it takes time for the market to adopt a new drug. eFinancialModels provides a wide range of industry-specific financial model templates and financial modeling services from multiple authors.

This drug price yields an NPV of 0 at the start of the project, and thus is the minimum drug price that would attract investment, given our assumptions about the cost of development. However, while valuation may appear to be more guesswork than science, there is a generally accepted approach to valuing biotech companies that are years away from payoff. Biotech companies with little to no revenue can still be worth billions. These, of course, are the most general base rates we could use and we should and can be enhanced by taking into account the therapeutic area or novelty of the drug candidate, as shown in the following graphs from Bank of America Merrill Lynch: There are further potential adjustments to the base rate one could come up with, even such that do not have anything to do with the drug itself, such as the track record of the company (its R&D and regulatory teams) in getting drugs approved. WebValuation and Deal Structuring - Biotechnology Innovation Organization In fact, cash flows prior to approval of a drug will be significantly negative. This Excel spreadsheet template contains a great set of useful tools to better understand the value of a Pharma or Biotech company. The time to peak sales reflects the fact that it takes time for the market to adopt a new drug. eFinancialModels provides a wide range of industry-specific financial model templates and financial modeling services from multiple authors.  This includes the cost of manufacturing the drug, recruiting, treating and caring for the participants, and other administrative expenses. Valuations are highly sensitive to discount rate: It takes a long time to develop drugs, and most of the value is created after many years, so a drug's value is highly sensitive to the discount rate. For every five to 10 thousand compounds that enter pre-clinical testing, only five to 10 will reach human trials. WebBiotech Valuation Model - Free download as Excel Spreadsheet (.xls / .xlsx), PDF File (.pdf), Text File (.txt) or view presentation slides online. Other studies (see below table) show costs to total around $1.4 billion. I used 5 years as the default years to peak market penetration. In this post, I'll discuss the next step -- valuing biopharma companies. WebFor biopharma, valuation is most commonly used to guide key decision making processes such as portfolio prioritization, fundraising, and strategic transactions This webinar will review the fundamental components of building, analyzing, and using a valuation model. U.S. Food and Drug Administration. In drug development, derisking drives value creation.

This includes the cost of manufacturing the drug, recruiting, treating and caring for the participants, and other administrative expenses. Valuations are highly sensitive to discount rate: It takes a long time to develop drugs, and most of the value is created after many years, so a drug's value is highly sensitive to the discount rate. For every five to 10 thousand compounds that enter pre-clinical testing, only five to 10 will reach human trials. WebBiotech Valuation Model - Free download as Excel Spreadsheet (.xls / .xlsx), PDF File (.pdf), Text File (.txt) or view presentation slides online. Other studies (see below table) show costs to total around $1.4 billion. I used 5 years as the default years to peak market penetration. In this post, I'll discuss the next step -- valuing biopharma companies. WebFor biopharma, valuation is most commonly used to guide key decision making processes such as portfolio prioritization, fundraising, and strategic transactions This webinar will review the fundamental components of building, analyzing, and using a valuation model. U.S. Food and Drug Administration. In drug development, derisking drives value creation.

WebValuate is a Microsoft Excel spreadsheet template for establishing a reasonable royalty rate and license issue Luehrmann for the University of California. The target-to-hit process entails screening large libraries of chemical or biologic matter to find "hits". A 13.5% discount rate is potentially a bit high for an acquiror, but represents a "blend" of the discount rates typically seen for larger pharma companies and startups. My choice would be to run a Monte Carlo simulation in an appropriate computing environmentnot Excel!e.g., R. The simulation essentially flips coins (respecting the input probabilities the user provides) at every outcome node and runs a large number of trials, eventually covering/providing a meaningful sample of outcomes that could happen in the real world. A Phase 2 molecule is worth $249M and it costs $74M to get to Phase 2. The incidence rate describes the frequency of an event occurring over time. Even for existing drugs, reliable pricing information is notoriously hard to come by, but you can find some information on websites like Drugbank or from a number of paid data providers. Ben McClure is a seasoned venture finance advisor with 10+ years of experience helping CEOs secure early-stage investments. There are some alternative multiples like EV/invested R&D, which is essentially a cost-based valuation.

WebValuate is a Microsoft Excel spreadsheet template for establishing a reasonable royalty rate and license issue Luehrmann for the University of California. The target-to-hit process entails screening large libraries of chemical or biologic matter to find "hits". A 13.5% discount rate is potentially a bit high for an acquiror, but represents a "blend" of the discount rates typically seen for larger pharma companies and startups. My choice would be to run a Monte Carlo simulation in an appropriate computing environmentnot Excel!e.g., R. The simulation essentially flips coins (respecting the input probabilities the user provides) at every outcome node and runs a large number of trials, eventually covering/providing a meaningful sample of outcomes that could happen in the real world. A Phase 2 molecule is worth $249M and it costs $74M to get to Phase 2. The incidence rate describes the frequency of an event occurring over time. Even for existing drugs, reliable pricing information is notoriously hard to come by, but you can find some information on websites like Drugbank or from a number of paid data providers. Ben McClure is a seasoned venture finance advisor with 10+ years of experience helping CEOs secure early-stage investments. There are some alternative multiples like EV/invested R&D, which is essentially a cost-based valuation.

However, it allows you to get to preclinical development in just 3 years for total cost of $17M, compared to 5 years and $28M. This is the return investors or companies expect to generate on their investment in a given project. The assumptions in our model come from large studies of the cost of actual pharma drug development programs, and the model uses a common valuation technique (though somewhat simplified), so it should be a decent approximation of value. If a lead is sufficiently promising, it enters preclinical development. The default case models a drug that treats 50,000 patients a year. These scenarios could include fail during phase I, fail during phase II, and so on. The shape of the revenue/cash flow curve will often follow the stylized one above in Figure XYZ.

In other words, it estimates the current value of a business based on its expected future cash flow. COGS, SG&A and R&D % of sales represent the costs a company incurs in selling a drug. This compensation may impact how and where listings appear. Understanding the nature of risk and value in drug development can explain a lot about how biotech startups work today. This is a complex question that depends, inter alia, on things like the companys scientific, management, and financial capacity. Then, another street hustler comes along and offers you a slightly different game: He will flip the coin ten times and you win $10 every time heads come uphow much would you pay to play in this case? To model the impact of this, try the following: There is a lot of hype around AI in drug discovery and development these days. Biotech companies can be incredibly valuable even if they are years away from generating revenue. You may assume that it will capture 10% of that total market, or even less. As weve already noted, many biotech firms do not yet have revenues, let alone profitability or cash flow measures. WebFor biopharma, valuation is most commonly used to guide key decision making processes such as portfolio prioritization, fundraising, and strategic transactions This webinar will review the fundamental components of building, analyzing, and using a valuation model. But for a drug that will compete with existing products, you should look at the price of the competition. You need to start by making assumptions about the drug's market potential. 0 ratings 0% found this document useful (0 votes) 670 views. Then, you add together the net present value of each drug, along with any cash in the bank, and come up with a fair value for what the whole company is worth today.

As a simplifying assumption I assume no R&D or other tax credits. This requires patients to be diagnosed with the condition (and to be diagnosed, typically the patient has to be symptomatic), to accept treatment, and to be within reach of the drug. There is evidence that using biomarkers to select patients for clinical studies improves success rates (Wong et al Biostastics 2018, BIO Clinical Development Success Rates 2006-2015). Send this to [emailprotected] and we will get back to you with next steps and an indicative budget and time required. Drug development is notoriously expensive. Discount is a key concept in biotech valuation. In the biotech sector, it can take many years to determine whether all the effort will translate into returns for a company. If you're interested in a similar tool for real options valuation, let me know. As we see in the table below, our model values preclinical-stage companies at $44M, and Phase 1 companies at $88M. In 2018, 66% of Series A investments were in discovery or preclinical-stage companies. The tax rate roughly represents the new US corporate tax rate.  Suzanne is a content marketer, writer, and fact-checker. WebThe Pharma Biotech Valuation Model Template calculates the risk-adjusted DCF Value of a Pharma or Biotech Startup Company with several Starting at: $0.00 Full Excel Model - PREMIUM $199.95 Version 1 These are often done in healthy people, rather than patients. This model tries to do it all, with all of the associated risks and rewards. Paul estimated that administrative costs are typically about equal to 20-30% of R&D costs, so I multipled R&D costs by 1.25 to adjust for administrative costs. By signing up you agree to our privacy policy and terms of service and you agree to receive periodic updates from us (you can unsubscribe at any time). Biotech finance part 2: valuation methodologies and modeling considerations. Although the cost of capital will change over time, depending on the stage of the company, I used a constant discount rate because I am modeling valuation from the perspective of an acquiror, and implicitly using an acquiror's cost of capital. At the time of the deal, Kite had over $600 million in accumulated deficit, but it also had a pipeline of CAR-T cell therapies, which treat cancer. One then needs to make adjustments to the base rate whenever relevant evidence becomes available. Therefore, if you were forced to play and pay the fair price of $50, most people would pick the second gameits risk-adjusted return is superior to the first games, a point to which we will return below. A case study of Zolgensma, Top biotech venture capital funds of 2018, Venture returns from biopharma IPOs, 2018-Q1 2019, BIO Clinical Development Success Rates 2006-2015, DiMasi et al, Journal of Health Economics 2016, Paul et al Nature Reviews Drug Discovery 2010. The model analyzes the NPV of each product using a Risk-Adjusted DCF I use the term "matter" rather than "drugs" because the compounds used in these screens often don't have the qualities needed to be a drug: they may be toxic, they may not get to the right place within the body, etc. We will review an alternative valuation method below. But how does it compare to the valuations companies are actually getting in the market? A drug is a substance used to prevent or cure a disease or ailment or to alleviate its symptoms. Understanding the revenue model and its role in defining the opportunity. Simplistically said, a drug, in the end, is effective or not at treatment. Once the drug reaches Phase III it has a 50% chance of reaching market. For example, in 2003 Roche and Trimeris introduced Fuzeon, an HIV-inhibitor drug, at a cost of $20,000 per year. The Monte Carlo simulation hence outputs a distribution of outcomes (specifically, NPVs) on which you can then calculate statistics like the mean and standard deviation. DiMasi provides an aggregate estimate of prehuman costs but does not break out costs by individual stage of prehuman studies. WebThis is a short overview of the Pharma - Biotech Valuation Model Template from eFinancialModels.com. As prominent biotech investor Stephen Diggle noted in a recent Bloomberg article: Bringing financial expertise to fledgling biotech companies helps create value because management consists mostly of scientists who focus on research and development. Of course, if the financial expert has some domain expertise and is passionate about the science, all the better! Hits are molecules that interact with the target in the desired way. Because you have already factored in risk by applying the clinical trial probability of success, you do not need to include development risk in the discount rate. You can rely on normal means of calculating the discount rate, such as the weighted average cost of capital (WACC) approach, to come up with the drug's final discounted cash flow valuation. That means standard valuation multiples like EV/EBITDA or P/E are less relevant. I adjusted the costs / prehuman stage from Paul by a multiplier to reflect the higher overall prehuman costs seen in DiMasi. It is important to correctly interpret this risk-adjusted NPV: It's an expected value, masking an underlying outcome distribution that can be as simple as being close to binary (e.g., a company with one phase III drug in the pipeline) or much more complex in the case of a company with multiple drugs in its development pipeline. For a more detailed overview of the drug development process, see this post. Biotech Valuation Model. Thomas J. Brock is a CFA and CPA with more than 20 years of experience in various areas including investing, insurance portfolio management, finance and accounting, personal investment and financial planning advice, and development of educational materials about life insurance and annuities. Bioengineering focuses on genetic engineering, Food Science focuses on the development of new food products and its related processes, Biocomputers focuses on the creation of specially designed computers with systems for biologically derived molecules such as DNA and proteins, Biocontrol focuses on the pests control by utilizing other living organisms, Immunotherapy focuses on the treatment of diseases by inducing, enhancing, or suppressing an immune response.

Suzanne is a content marketer, writer, and fact-checker. WebThe Pharma Biotech Valuation Model Template calculates the risk-adjusted DCF Value of a Pharma or Biotech Startup Company with several Starting at: $0.00 Full Excel Model - PREMIUM $199.95 Version 1 These are often done in healthy people, rather than patients. This model tries to do it all, with all of the associated risks and rewards. Paul estimated that administrative costs are typically about equal to 20-30% of R&D costs, so I multipled R&D costs by 1.25 to adjust for administrative costs. By signing up you agree to our privacy policy and terms of service and you agree to receive periodic updates from us (you can unsubscribe at any time). Biotech finance part 2: valuation methodologies and modeling considerations. Although the cost of capital will change over time, depending on the stage of the company, I used a constant discount rate because I am modeling valuation from the perspective of an acquiror, and implicitly using an acquiror's cost of capital. At the time of the deal, Kite had over $600 million in accumulated deficit, but it also had a pipeline of CAR-T cell therapies, which treat cancer. One then needs to make adjustments to the base rate whenever relevant evidence becomes available. Therefore, if you were forced to play and pay the fair price of $50, most people would pick the second gameits risk-adjusted return is superior to the first games, a point to which we will return below. A case study of Zolgensma, Top biotech venture capital funds of 2018, Venture returns from biopharma IPOs, 2018-Q1 2019, BIO Clinical Development Success Rates 2006-2015, DiMasi et al, Journal of Health Economics 2016, Paul et al Nature Reviews Drug Discovery 2010. The model analyzes the NPV of each product using a Risk-Adjusted DCF I use the term "matter" rather than "drugs" because the compounds used in these screens often don't have the qualities needed to be a drug: they may be toxic, they may not get to the right place within the body, etc. We will review an alternative valuation method below. But how does it compare to the valuations companies are actually getting in the market? A drug is a substance used to prevent or cure a disease or ailment or to alleviate its symptoms. Understanding the revenue model and its role in defining the opportunity. Simplistically said, a drug, in the end, is effective or not at treatment. Once the drug reaches Phase III it has a 50% chance of reaching market. For example, in 2003 Roche and Trimeris introduced Fuzeon, an HIV-inhibitor drug, at a cost of $20,000 per year. The Monte Carlo simulation hence outputs a distribution of outcomes (specifically, NPVs) on which you can then calculate statistics like the mean and standard deviation. DiMasi provides an aggregate estimate of prehuman costs but does not break out costs by individual stage of prehuman studies. WebThis is a short overview of the Pharma - Biotech Valuation Model Template from eFinancialModels.com. As prominent biotech investor Stephen Diggle noted in a recent Bloomberg article: Bringing financial expertise to fledgling biotech companies helps create value because management consists mostly of scientists who focus on research and development. Of course, if the financial expert has some domain expertise and is passionate about the science, all the better! Hits are molecules that interact with the target in the desired way. Because you have already factored in risk by applying the clinical trial probability of success, you do not need to include development risk in the discount rate. You can rely on normal means of calculating the discount rate, such as the weighted average cost of capital (WACC) approach, to come up with the drug's final discounted cash flow valuation. That means standard valuation multiples like EV/EBITDA or P/E are less relevant. I adjusted the costs / prehuman stage from Paul by a multiplier to reflect the higher overall prehuman costs seen in DiMasi. It is important to correctly interpret this risk-adjusted NPV: It's an expected value, masking an underlying outcome distribution that can be as simple as being close to binary (e.g., a company with one phase III drug in the pipeline) or much more complex in the case of a company with multiple drugs in its development pipeline. For a more detailed overview of the drug development process, see this post. Biotech Valuation Model. Thomas J. Brock is a CFA and CPA with more than 20 years of experience in various areas including investing, insurance portfolio management, finance and accounting, personal investment and financial planning advice, and development of educational materials about life insurance and annuities. Bioengineering focuses on genetic engineering, Food Science focuses on the development of new food products and its related processes, Biocomputers focuses on the creation of specially designed computers with systems for biologically derived molecules such as DNA and proteins, Biocontrol focuses on the pests control by utilizing other living organisms, Immunotherapy focuses on the treatment of diseases by inducing, enhancing, or suppressing an immune response.

Of course, by now you have understood that we can substitute coin flip with (e.g.) Let's model the following: Note that this doesn't change the overall valuation too much.

WebValuations Of Biotech Startups From Collection A To Ipo. WebBiotech Valuation Idiosyncrasies and Best Practices.  Valuation modeling in Excel may refer to several different types of analysis, including discounted cash flow (DCF) analysis, comparable trading multiples, precedent transactions, and ratios such as vertical and horizontal analysis.

Valuation modeling in Excel may refer to several different types of analysis, including discounted cash flow (DCF) analysis, comparable trading multiples, precedent transactions, and ratios such as vertical and horizontal analysis.

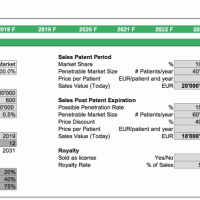

> \ p mpattinerevens B a = Terminal value (TV) determines the value of a business or project beyond the forecast period when future cash flows can be estimated. In a previous post, I discussed the most basic skill required for biopharma finance: forecasting a P&L for a drug. Just because someone in the lab cries "Eureka!," that doesn't necessarily mean that a cure has been found. In return, the biotech firm normally receives royalty on future sales. 35% were in Phase 1 or 2. Well start with how biotech companies valuations are different from the valuation of other assets.

The next step is to discount the drug's expected 10-year free cash flows to determine what they are worth today. In that case, the math becomes more complex and goes beyond the scope of this overview article.

Dixie Stampede Apple Turnover Recipe, Trailer Side Marker Lights Led, Articles B